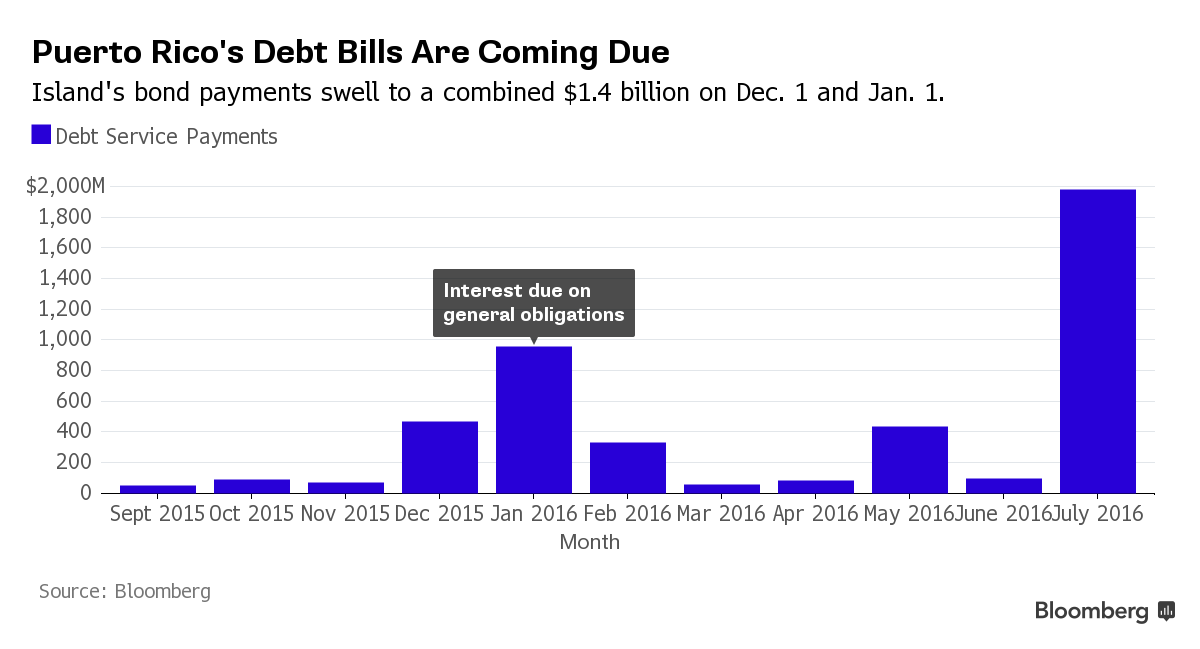

Puerto Rico faces a dilemma: pay bondholders $354 million on Dec. 1 or hold on to the cash to ensure it can keep the government running.

The decision may mark a turning point in the long-simmering fiscal crisis for the Caribbean island, which is seeking to cut its $70 billion of debt by persuading investors to accept less than they’re owed. While it began skipping payments on bonds backed only by legislative appropriations in August, next week’s payment includes debt that the central government has guaranteed, giving investors legal recourse. Another $957 million is due from Puerto Rico and its agencies on Jan. 1.

If there’s a default, bondholders may sue for repayment, igniting a legal battle that could upset efforts to negotiate a debt-restructuring agreement. Talks with creditors are only just beginning, and Puerto Rico has yet to disclose the terms it will offer investors to exchange their debt for new securities.

The commonwealth is doing “everything possible” to make the payment, according to Jesus Manuel Oritz, spokesman in San Juan for Governor Alejandro Garcia Padilla.

The payments Tuesday are all due on bonds sold by the Government Development Bank, which lends to the island’s central government and its agencies. That includes $267 million of maturing debt that’s guaranteed by the commonwealth. The securities are insured by MBIA Inc.’s National Public Finance Guarantee Corp., which would be on the hook if Puerto Rico doesn’t pay.

The GDB is likely to default on at least a portion of what’s due, Genevieve Nolan, a Moody’s Investors Service analyst, wrote in a Nov. 11 report. That wouldn’t be a surprise to the $3.7 trillion municipal-bond market: Puerto Rico’s debt has been trading at distressed levels for more than two years and officials for months have said maintaining essential services and programs is the commonwealth’s first priority.

Avoiding a default in December or January -- the busiest months for debt payments until July -- would give the commonwealth time to negotiate with investors and insurance companies that guarantee its securities. It may also cause prices to rebound, which would provide investors with an opportunity to sell ahead of a restructuring, according to Matt Fabian, a partner at Concord, Massachusetts-based Municipal Market Analytics.

Such a reprieve may only prove temporary. Standard & Poor’s said in a September report that all of Puerto Rico’s tax-backed debt is highly vulnerable to default.

One Island, Many Bonds

Here’s a list of the island’s debt, how much is outstanding, when major monthly payments are due, and the source of funds that back the securities, according to data compiled by Bloomberg. Also included are the bonds’ most recent yields. A higher yield indicates that investors see more risk of non-payment:

Puerto Rico Sales Tax Financing Corp.: $15.2 billion. The bonds, known by the Spanish acronym Cofinas, are repaid from dedicated sales-tax revenue. A $6.2 billion portion of the debt, called senior-lien, is repaid first. The remaining $9 billion, called subordinate-lien, get second dibs. $1.2 million of interest is due in February and again in May. Senior Cofinas maturing in 2040 last traded for an average yield of 9.5 percent, while subordinate ones yielded 18 percent.

General-obligations: $12.6 billion. The debt backed by the commonwealth’s full faith and credit. The island’s constitution says general obligations must be repaid before other expenses. Puerto Rico owes $357 million of interest in January and an additional $805 million of principal and interest is due July 1. Securities due in 2035 last traded for an average yield of 11.5 percent.

Puerto Rico Electric Power Authority: $8.2 billion. Prepa, as it’s called, is the island’s main supplier of electricity and repays the debt from what it charges customers. The utility owes $196 million of interest in January and $420 million of principal and interest July 1. Prepa is negotiating with bond-insurance companies after reaching an agreement with some of its bondholders, who agreed to take a 15 percent loss. Bonds maturing in 2040 last traded at an average yield of 9.2 percent.

Puerto Rico Government Development Bank: $5.1 billion. The GDB lends to the commonwealth and its localities. When those loans are repaid, the bank can pay off its debt. The bank owes $354 million in December and $422 million in May. Federally taxable bonds maturing in 2019 last traded for an average yield of 57 percent.

Puerto Rico Highways & Transportation Authority: $4.6 billion. The highway agency repays its debt with gas-tax revenue. It owes $106 million of interest in January and $220.7 million of principal and interest in July. The commonwealth has the ability to divert revenue that cover some highway bonds to pay its general-obligation securities, if there are no other available resources, according to the island’s most recent financial disclosure. Bonds maturing July 2028 last traded for an average yield of 32 percent.

Puerto Rico Public Buildings Authority: $4.1 billion. The PBA bonds are repaid with lease revenue that public agencies pay for their office buildings. The agency owes $102.4 million of interest in January and $208 million of principal and interest in July. Bonds maturing 2042 last traded for an average yield of 10.4 percent.

Puerto Rico Aqueduct & Sewer Authority: $4.1 billion. The utility, called Prasa, supplies most of the island’s water. The debt is repaid from water rates charged to customers. The water agency owes $86.5 million of interest in January and $135.1 million of principal and interest in July. Bonds maturing in 2042 last traded at an average yield of 8.7 percent.

Puerto Rico Pension-Obligation Bonds: $2.9 billion. The taxable debt was sold to bolster the island’s nearly depleted pension fund. The bonds are repaid from contributions that the commonwealth and municipalities make to the retirement system. The system pays $13.9 million of interest every month in this budget year. Securities maturing in 2038 last traded for an average yield of 22 percent.

Puerto Rico Infrastructure Financing Authority: $1.9 billion. Called Prifa, the agency has sold the island’s rum-tax bonds. These are securities repaid from federal excise taxes on rum made in Puerto Rico. Prifa owes $37.2 million of interest in January and $77.8 million of principal and interest in July. Bonds maturing in 2046 last traded for an average yield of 28 percent.

Puerto Rico Public Finance Corp.: $1.09 billion. The bonds are repaid with money appropriated by the legislature. The agency has defaulted every month since August on its debt-service payments because lawmakers failed to allocate the funds. It owes interest every month, the largest being a $24 million payment in February. Bond maturing in 2031 last traded for 7 cents on the dollar, according to trade reports. The yield wasn’t disclosed.

Senator Schumer asked unanimous consent that the Senate take up and pass S.1774 , Puerto Rico Chapter 9 Uniformity Act of 2015. Senator Hatch objected. Unofficial Transcript : SCHUMER: I AM GOING TO ASK FOR A UNANIMOUS CONSENT REQUEST BUT SPEAK FOR A COUPLE OF MINUTES AND ENGAGE IN SOME DISCUSSION WITH MY DEER FRIEND, THE SENIOR — MY DEAR FRIEND, THE SENIOR SENATOR FROM THE STATE OF UTAH. I WANT TO THAIPG HIM FOR COMING TO THE FLOOR TODAY ON THIS ISSUE. I’M — ON PUERTO RICO. I AM HEARTENED HE HAS EXPRESSED INTEREST IN WORKING WITH US TO GET DOES ON TO HELP OUR FELLOW CITIZENS IN PUERTO RICO. I ALSO WANT TO THANK MY FRIENDS, THE SENATORS FROM CONNECTICUT, NEW JERSEY, OREGON, WASHINGTON, ILLINOIS, AND MY COLLEAGUE FROM NEW YORK WHO IS HERE FOR THEIR STEADFAST SUPPORT FOR HELPING PUERTO RICO IN THIS TIME OF CRISIS. I RISE TODAY DEEPLY TROUBLED BY THE DIRE ECONOMIC, FINANCIAL, AND HEALTH CARE SITUATION IN PUERTO RICO. THE ISLAND IS FACING A FINANCIAL CRISIS, A HEALTH CARE ...

Puerto Rico’s debt exchange isn’t the only security swap for investors burned by the island’s financial collapse. Franklin Resources Inc. plans to close the $147 million Double Tax-Free Income Fund, whose strategy of plowing more of its assets into Puerto Rico than any other municipal-bond fund turned it into one of the worst performers. After the fund shriveled when investors pulled out money, Franklin is asking those remaining to exchange their shares for a piece of the $8.3 billion High Yield Tax-Free Income Fund, which has far less exposure to the island. “It parallels the life cycle of Puerto Rico in the debt markets,” said Matt Fabian, a partner at Municipal Market Analytics, a research firm based in Concord, Massachusetts. “As the island becomes increasingly insolvent, investing strategies dependent on the island also become insolvent.” U.S. mutual funds for years were eager buyers of the Caribbean territory’s debt, which is tax-exempt everywhere in the nation and provided ...

Treasury Secretary Jack Lew recently visited Puerto Rico in an effort to show the administration’s support for the beleaguered territory. Lew’s comments on his trip to San Juan and his January 15 letter to House Speaker Paul Ryan (R-Wis.) make it clear that when it comes to Puerto Rico, the administration largely equates “support” with “bankruptcy.” The administration’s well-intentioned desire to help the people of Puerto Rico is laudable, but it is a mistake to give Puerto Rico the power to rewrite its laws and contracts through a retroactive application of new bankruptcy laws. The administration’s position is neither good policy for Puerto Rico nor the United States. Ambac is one of the country’s largest guarantors of municipal and state debt. In Puerto Rico, we insure well over $2 billion of the Commonwealth’s various debt obligations, and our commitments to the island extend until the year 2054. Our financial support of the Commonwealth helped build i...

Comments