Puerto Rico’s debt exchange isn’t the only security swap for investors burned by the island’s financial collapse.

Franklin Resources Inc. plans to close the $147 million Double Tax-Free Income Fund, whose strategy of plowing more of its assets into Puerto Rico than any other municipal-bond fund turned it into one of the worst performers. After the fund shriveled when investors pulled out money, Franklin is asking those remaining to exchange their shares for a piece of the $8.3 billion High Yield Tax-Free Income Fund, which has far less exposure to the island.

“It parallels the life cycle of Puerto Rico in the debt markets,” said Matt Fabian, a partner at Municipal Market Analytics, a research firm based in Concord, Massachusetts. “As the island becomes increasingly insolvent, investing strategies dependent on the island also become insolvent.”

U.S. mutual funds for years were eager buyers of the Caribbean territory’s debt, which is tax-exempt everywhere in the nation and provided high yields in a municipal market that’s known as a haven. With Puerto Rico pushed to the brink, that investment tactic has turned toxic: The five worst-performing open-ended municipal funds in the past year, including Franklin’s, all had at least 10 percent of their assets in the island’s securities, according to Bloomberg and Morningstar Inc. data.

Puerto Rico, which racked up $70 billion of debt by routinely borrowing to paper over budget shortfalls, has already skipped interest payments on some securities and may default on general-obligation bonds for the first time by July. Governor Alejandro Garcia Padilla is seeking to cut what the commonwealth owes by about 46 percent by asking investors to exchange their bonds for new securities. If they decline, his administration has said it may suspend interest and principal payments altogether.

The anticipated losses from the island’s building crisis caused the price of Puerto Rico bonds to tumble over the past two years. Securities due in 2035, the most frequently traded, have dropped to about 71 cents on the dollar, down 24 percent since they were first sold to investors in March 2014.

Franklin, which has about $1.6 billion of commonwealth securities among its municipal funds, is one of Puerto Rico’s biggest bondholders. The San Mateo, California-based company, along with BlueMountain Capital Management and OppenheimerFunds, successfully sued to overturn a Puerto Rico law that would allow the government to cut its debts, similar to how U.S. cities can in bankruptcy proceedings. The U.S. Supreme Court will hear arguments on March 22 about whether that law should be reinstated.

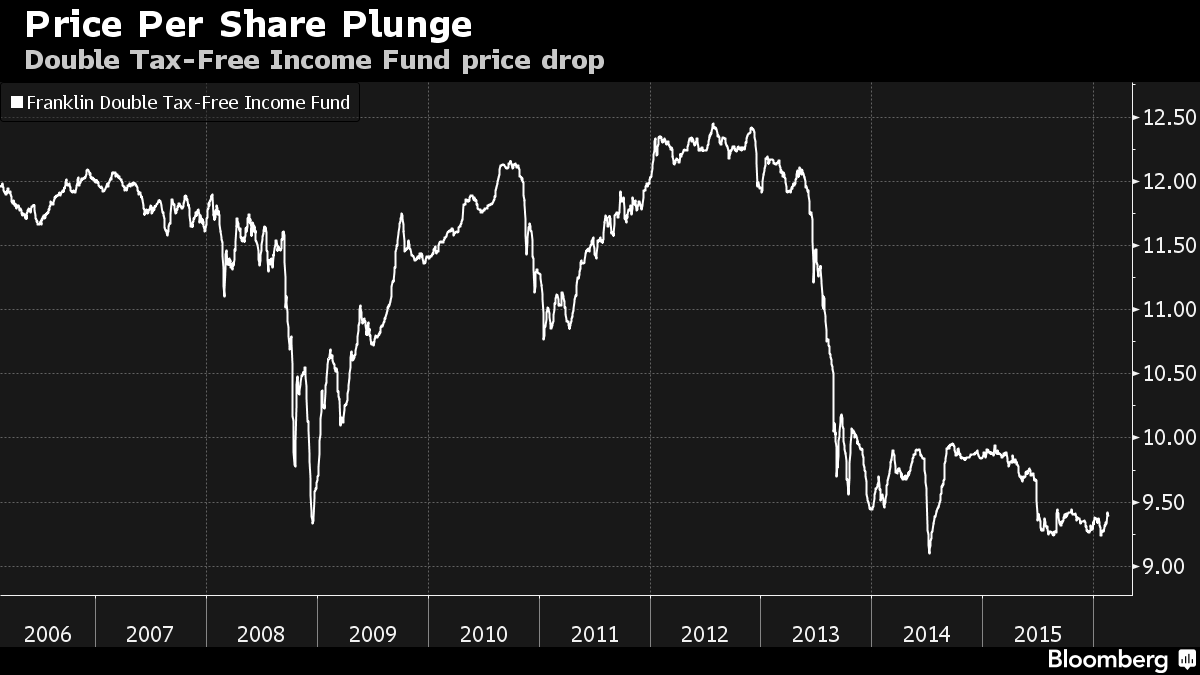

The Double Tax-Free fund, which was started in 1985 and focuses on debt issued by U.S. territories, was among the funds hardest hit as the island veered toward default, and it has been closed to investors since August 2012. Its assets have dropped by 83 percent since July 2012, when it had $868.7 million, according to data compiled by Bloomberg. Almost half of its investments were Puerto Rico securities as of Jan. 31, according to the firm’s website. With the island locked out of the bond markets, the supply of territory bonds has been curtailed.

Advantages Seen

The proposed merger will offer Double Tax-Free shareholders “the opportunity to reorganize into a fund with a larger asset size, lower annual fund operating expenses, better long-term total return investment performance (although a slightly lower income return performance), and a more stable and diversified investment portfolio,” Stacey Johnston Coleman, a spokeswoman for Franklin, said in an e-mail.

The fund lost 1.1 percent in 2015, putting it at the very bottom percentile of performers, according to data compiled by Bloomberg. Its shares traded for $9.38 on Monday, down from as much as $12.27 in 2012.

If Double Tax-Free shareholders approve the merger at a meeting set for April 4, they’ll be given shares of the larger fund, which offers a more diverse mix of municipal bonds. If the step is rejected, the fund’s assets may be sold off and its money returned.

The average annual total return in the past 10 years for the Double Tax-Free fund was 2.07 percent, compared with 4.79 percent for the High Yield fund, according to Franklin’s website.

The merger would increase the High Yield funds’ allocation to Puerto Rico. It directed 3.1 percent, or about $258.8 million, to commonwealth securities, as of Jan. 31. Based on those amounts, the fund would have about 3.9 percent of its assets in the island’s debt if it absorbed all of the smaller portfolio.

That wouldn’t be a large increase to its Puerto Rico exposure, said Beth Foos, a senior analyst in Chicago at Morningstar who focuses on municipal mutual funds.

“You’re most likely gaining more stability and absorbing that stress and volatility into a much larger pool of assets,” she said. “If it were to go anywhere, this is the fund where it would make the most sense.”

Treasury Secretary Jack Lew recently visited Puerto Rico in an effort to show the administration’s support for the beleaguered territory. Lew’s comments on his trip to San Juan and his January 15 letter to House Speaker Paul Ryan (R-Wis.) make it clear that when it comes to Puerto Rico, the administration largely equates “support” with “bankruptcy.” The administration’s well-intentioned desire to help the people of Puerto Rico is laudable, but it is a mistake to give Puerto Rico the power to rewrite its laws and contracts through a retroactive application of new bankruptcy laws. The administration’s position is neither good policy for Puerto Rico nor the United States. Ambac is one of the country’s largest guarantors of municipal and state debt. In Puerto Rico, we insure well over $2 billion of the Commonwealth’s various debt obligations, and our commitments to the island extend until the year 2054. Our financial support of the Commonwealth helped build i...

Senator Schumer asked unanimous consent that the Senate take up and pass S.1774 , Puerto Rico Chapter 9 Uniformity Act of 2015. Senator Hatch objected. Unofficial Transcript : SCHUMER: I AM GOING TO ASK FOR A UNANIMOUS CONSENT REQUEST BUT SPEAK FOR A COUPLE OF MINUTES AND ENGAGE IN SOME DISCUSSION WITH MY DEER FRIEND, THE SENIOR — MY DEAR FRIEND, THE SENIOR SENATOR FROM THE STATE OF UTAH. I WANT TO THAIPG HIM FOR COMING TO THE FLOOR TODAY ON THIS ISSUE. I’M — ON PUERTO RICO. I AM HEARTENED HE HAS EXPRESSED INTEREST IN WORKING WITH US TO GET DOES ON TO HELP OUR FELLOW CITIZENS IN PUERTO RICO. I ALSO WANT TO THANK MY FRIENDS, THE SENATORS FROM CONNECTICUT, NEW JERSEY, OREGON, WASHINGTON, ILLINOIS, AND MY COLLEAGUE FROM NEW YORK WHO IS HERE FOR THEIR STEADFAST SUPPORT FOR HELPING PUERTO RICO IN THIS TIME OF CRISIS. I RISE TODAY DEEPLY TROUBLED BY THE DIRE ECONOMIC, FINANCIAL, AND HEALTH CARE SITUATION IN PUERTO RICO. THE ISLAND IS FACING A FINANCIAL CRISIS, A HEALTH CARE ...

Comments